Whether you are seeking a home appraisal because you are buying, refinancing, or selling a home, it is important to understand the information on your home appraisal report.

Many buyers obtain a home appraisal out of obligation and give it nothing more than a cursory glance. Anyone who hopes to be successful at real estate investing, however, should become comfortable with analyzing their report.

What Is an Appraisal Report?

Unlike home inspections, the home appraisal is not about looking for safety issues and potential system problems. The licensed, unbiased third-party appraiser is there to determine the value of the property.

You can download the appraisal report we used to create this tutorial here. We will attempt to create a tutorial below for each section of it.

When assessing the value of real estate, there are four elements to consider: demand, utility, transferability, and scarcity. An appraiser can use three main approaches to assess how your home meets these four requirements. The approach depends heavily on the purpose of the property.

Appraisals for residential homes typically use the sales comparison approach (sometimes called market data analysis). This approach factors in the location and compares the value of other homes in the area.

For special-use properties such as churches and schools, the cost replacement approach is used. This approach considers how much it would cost to completely rebuild that property and bases its value on the replacement cost.

Another approach is the income capitalization approach, which bases the value on the income the property will generate. This approach is likely to be applied for an investment property.

Understanding the 1004 Form

If you are applying for a mortgage or refinancing your home, your appraiser will most likely use the Uniform Residential Appraisal Report (1004 form). This form covers all the key components that are essential to determining the property value.

While it may not be the most exciting reading material, getting familiar with each section will help you become a better investor.

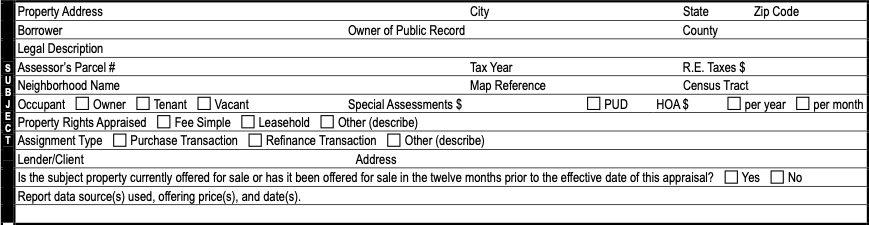

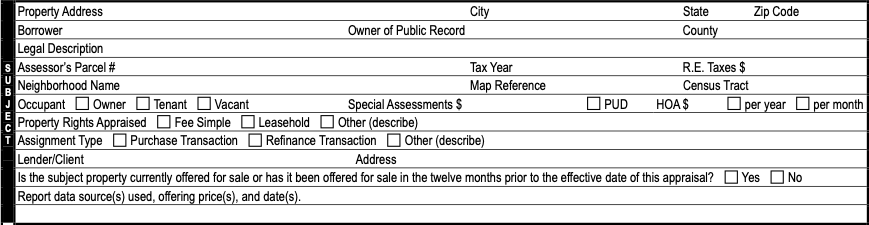

Subject

The first section of the 1004 (often called the “ten oh four form”) is titled “Subject,” and it contains information about the borrower. It covers whether the owner of the property has full ownership, who occupies the property, and the reason for the appraisal.

The type of assessment to be done can vary depending on whether this is a purchase transaction or a refinance transaction, so those details are noted in this section as well.

Contract

The next section is titled “Contract,” and it covers important details of the contract like the financial details. The appraiser will verify they have read the contract and add the contract amount to the report. This is the part of the report where any financial assistance will be specified.

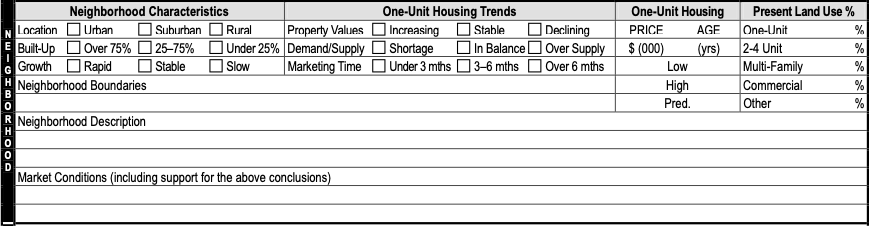

Neighborhood

The third section is titled “Neighborhood,” and this is the area where the value of the property is assessed. Is the property location considered urban, suburban, or rural? Is the neighborhood upwardly or downwardly mobile? What is the demand for homes in this location?

An appraiser may take a spin around the neighborhood and quickly assess similar homes. Home values can be micro-local and vary wildly from one street to the next, so it is ideal to have an appraiser who is very familiar with the area. Other things to examine are the quality of the school district, the crime rate, and the walkability of the location.

The condition of the surrounding homes is considered; presentable neighborhoods generate a higher value for your home. It is a sad reality that you can purchase a home when an area is thriving and then, due to external factors, the surrounding area can deteriorate.

When a property loses value due to its neighborhood becoming undesirable, it is called “economic obsolescence.” This is the worst fear of many investors who’ve held on to their investment long term.

Be sure to do thorough research on any prospective investment’s location and pay attention to trends in the area. If local businesses are closing down and crime is rising, it may be best to look elsewhere.

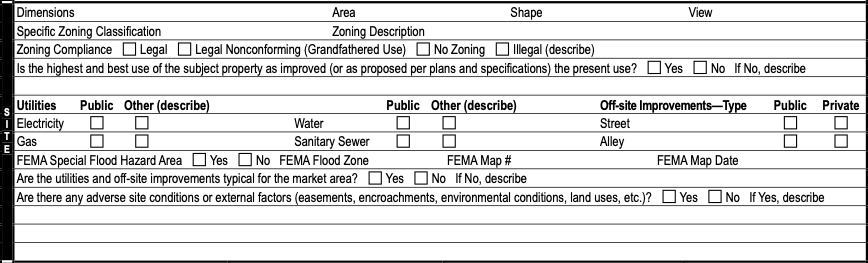

Site

The appraiser will also record the zoning classification and description in the section titled “Site.” What utilities the property is zoned for, the intended use of the property, and its current use are also noted in this section. The focus here is that the property fits legal use.

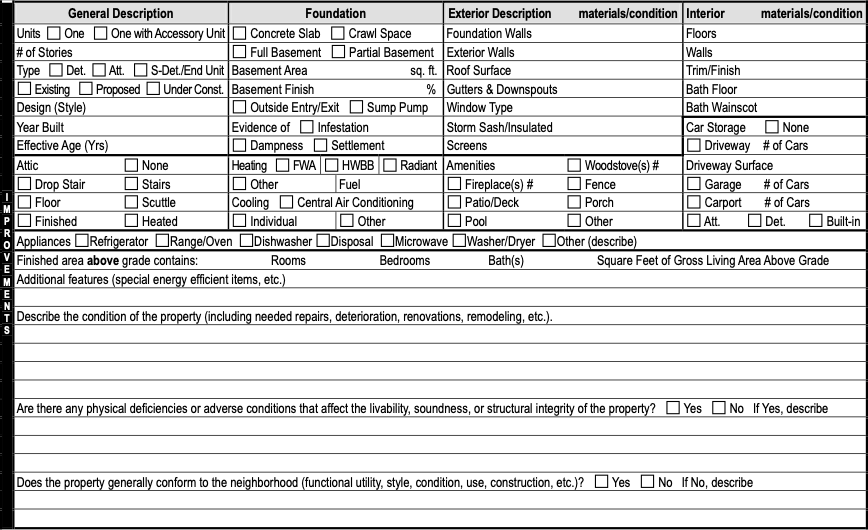

Improvements

In the “Improvements” section, the features of the property are noted, along with any improvements or additions that have been done. While improvements and amenities may add to your enjoyment of your home, don’t expect them to automatically improve your property value.

You know that fancy new pool you insisted on adding to the backyard? It may be meaningless when it comes to your report. The value of upgrades are in the eye of the beholder and may be of little interest to a prospective buyer. Your upkeep of home maintenance is already expected and whether the material you used was high or low quality matters little.

Decor and style are also inconsequential as trends changes rapidly. The condition of the property, repairs needed, and adverse conditions that may affect the structure are the main concerns in this section of the report.

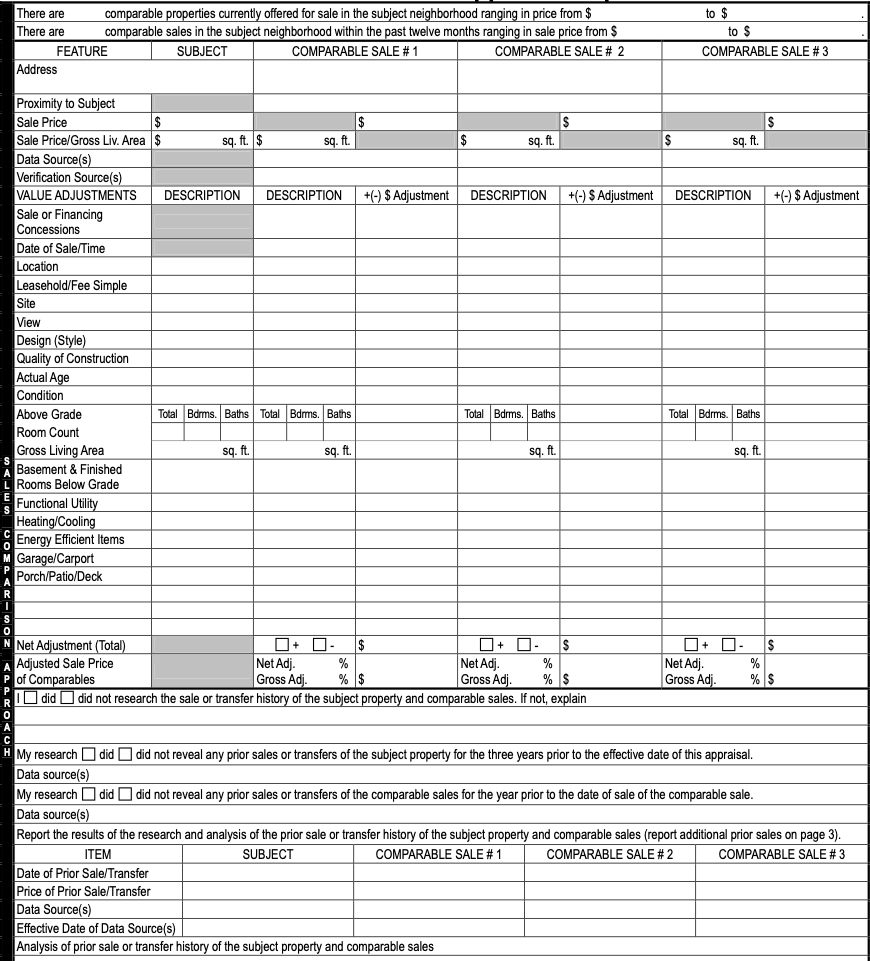

Sales Comparison Approach

On the next page, there is a section for the appraiser to list at least three properties that are similar to your home. They must be located within a close radius and have been sold recently. To get the most accurate comparison, Forest Selby of The Firehill Group recommends that comparable properties from within the same geographic location should have sold within the last 30-90 days.

The appraiser will research other properties in the area that are comparable to yours, adjusting any differentials, and this information will be applied to the report. Recent appraisals for similar homes in the area will be helpful if available in the county’s Record of Deeds. Official records are the best data source for comparable properties because, unlike Zillow and other listing sites, information cannot be added by just anyone.

While Zillow can be a great starting point for appraisal research, most professionals prefer to stick to official assessments recorded with the county. If an appraiser is using the sales comparison approach but cannot find any similar sales for comparable properties, they will have to use the cost replacement approach.

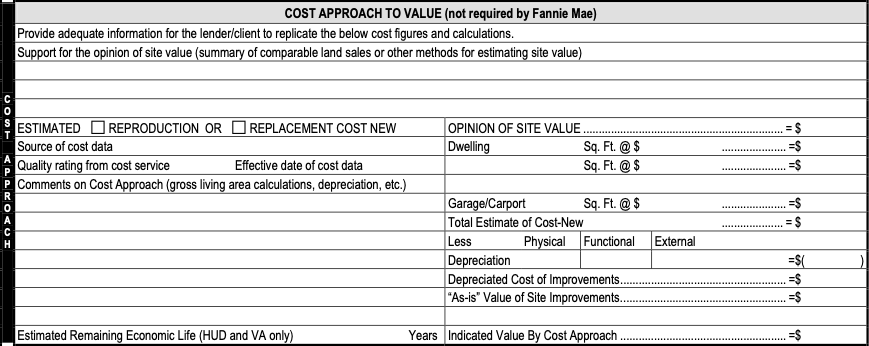

Cost Replacement Approach

The cost replacement approach has a small section on the report, and an appraiser may or may not choose to fill it in. If this approach is used, the appraiser will examine exactly how much it would cost to build the home or building if it had to be replaced.

No comparisons are used for this approach. It is a common approach to use for properties that are one of a kind or very old and therefore do not have easy comparisons.

Income Capitalization Approach

The income capitalization approach is the next section and, while not required by most mortgage companies, it is valuable to many investors. It calculates the potential monthly income of a property based on current market data.

If you purchase a home for $100,000 and you charge $1,000 per month in rent, you will divide 100,000 by 1,000 to find your monthly gross rent multiplier, which is 100. To find your annual gross rent multiplier, just multiply $1,000 by 12 months, divide 12,000 into 100,000, and your gross rent multiplier is 8.3.

This information is important for rental properties, and so many investors require this section to be filled out for their report. There is an additional field for PUD homes and, if applicable, this is where the specifics of the homeowners association would be noted.

Appraisal Results

If all goes well, your appraisal will come back at or above value “as is.” This means they have reached the value based on the condition the property is currently in.

It may come back as “subject to.” In this case, the appraiser has given you the value of your property factoring in some improvements that you must make. Once you have made these improvements, your home will be valued at the amount specified.

If you believe that the value of your appraisal is incorrect, you can dispute the outcome by sending a reconsideration of value request letter to your lender. Incorrect values can occur when the comparable properties were not adequate, especially if the appraiser is not familiar with the area.

Contingencies can be useful if set up ahead of time. For example, you as the buyer can agree prior to the assessment that if the value comes back lower than the negotiated purchase price, you are released from the deal.

It typically takes about a week for the appraiser to complete the report of your home’s value. Regardless of the reason you are having the appraisal done, it is important that you keep a copy of the report for your records. It ensures that negotiations and discussions will be fair to all parties and is a tangible representation of your investment.